Some Prediction Markets for the 2024 Election

Arbitrage opportunities galore!

Hello everyone. In this post I’m going to walk through a 100 or so markets I made on Manifold in the 2024 US Presidential Election topic (most of them as a part of larger unlinked multi-choice markets).

The point of these markets is to set up a sequence of arbitrage opportunities which will hopefully improve the accuracy of the bottom-line probabilities on which party will win the presidency.

It’s opined by political gamblers that top-line markets like this are often much less accurate than more esoteric markets like state-by-state results, because the former attract dumb money. My hope is to try to bridge this gap with new paths for arbitrage that let the top-line markets discover price better.

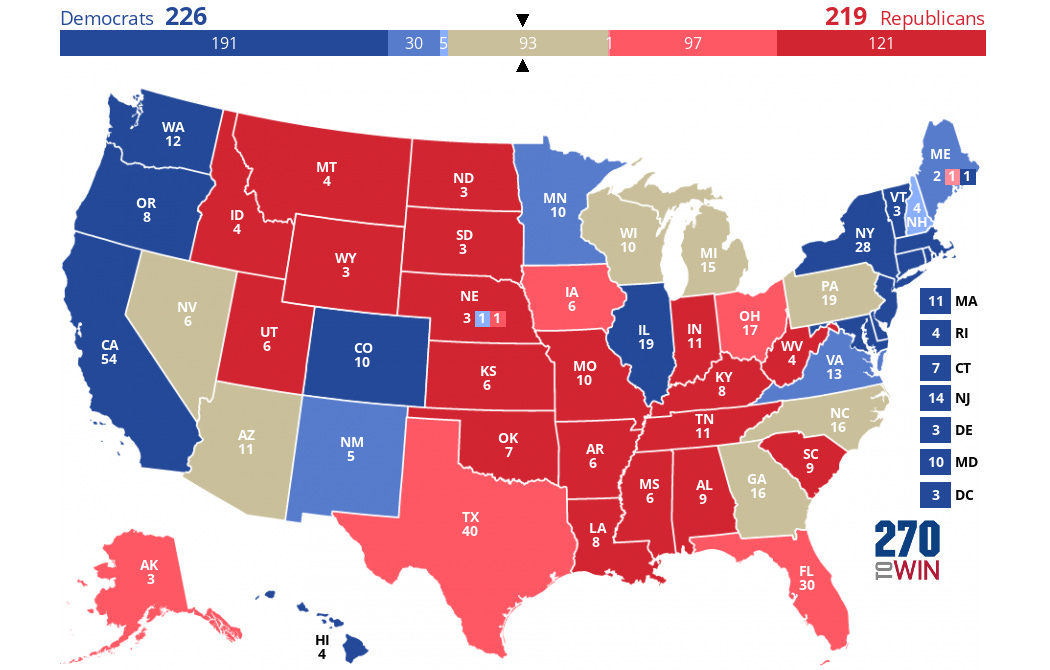

Which states to consider?

I decided to focus on just seven states when making my markets - the states listed as “toss-up” (in beige) in this map:

The advantage of limiting the number of states is that I can ask the market to more carefully consider outcomes for subsets of the states without dealing with combinatorial explosion. There are 50 states and 6 non-state territories that assign electoral votes separately. If I were to make a separate binary market even for just every pair of distinct electoral territories, I would need 1540 different markets.

With seven states, I can easily make a separate market to gauge the correlation of each pair (which will be important later on in this post). There is also the fortuitous coincidence that Georgia and North Carolina have the same number of electoral votes (16), and that Wisconsin and Nevada together also have exactly 16 electoral votes. So even though there are 128 distinct state-by-state outcomes among these seven, there are only 60 possibilities for electoral vote totals - a small enough number that I am comfortable making a multi-choice market for each one.

Do these states tell the whole story?

The main market from my cohort tries to approximate the general election with a simpler “hypothetical” election. In the hypothetical, every non-toss-up state goes as expected, and the seven toss-ups go the same way as they will in real life. I ask what the outcome would be in this world:

This is related to the target general election market by a load-bearing joint market that asks if this will resolve the same as the ultimate election outcome market.

I have bet the unlikely outcomes in the joint market second market down to a total of 4%, and then again down to 7% after others bet them back up. These bets were based on the following reasoning:

If all of the states marked as leaning red or blue do go as expected, then the markets will resolve the same by definition. This already seems fairly likely: At time of writing, the assessment of Metaculus is that the blue-leaning state which is most likely to go Republican is New Hampshire, with an estimated probability of 10%, and the red-leaning state which is most likely to go Democrat is Ohio, with an estimated probability of 6%. Certainly it was also true of the 2020 election (and also the 2016 election if you ignore Nebraska’s districts).

If some states that are currently leaning red or blue do not go as expected, the most likely explanation would be a somewhat strong red-wave or blue-wave scenario. Given that, it seems likely that the toss-up states will move with this wave and that the electoral college votes among them will end up on the correct side of predicting the nationwide totals.

Even in the event that there is a one-off fluke where a state like New Hampshire or Ohio does not go as expected, it is still possible for the markets to resolve the same, as long as the additional votes from the fluke state do not push the total over 270.

Another way of trying to estimate this is to look at 538’s 2020 election simulation interactive to get a sense of the chances of the hypothetical wrongly predicting the reality for that election.

538 gave around an 84% chance that Biden would win PA. If he did, he was 99% to win MI and WI, and a 99% chance to win the election with all of those, so the hypothetical would almost certainly have been right there.

On the other hand, if Biden lost PA, he had around 70% to lose GA and NC too, and only a 18% to win in that sub case.

Even if the remainder of the time the chance of winning was always 50%, this still makes for a 5% chance of the toss-up states calling it wrong. To be fair though, the frozen model which gives these numbers gives a baseline 89% chance of Biden winning, whereas the probability we now have for 2024 is closer to 50%, so it’s not an apples-to-apples comparison here. I welcome traders to share their opinion by commenting.

Regardless, there is the further happy conclusion that even if these unlikely outcomes are less unlikely than I think, it is still not obvious which one is less unlikely. So even if the pricing of these unlikely outcomes is wrong, the effect may partially cancel out so that the assessment of the final outcome is still accurate.

Electoral college analysis of the Toss-up states

Let’s further analyze the hypothetical world with the mixture of real results for toss-ups and expected results for non-toss-ups. As the map above kindly tells us, the Democratic candidate needs 270 votes to win the election1. The convenience of assuming the expected results is that we immediately know how 445 out of 538 electoral votes will go, leaving us to understand the possibilities for the remaining 93.

The easiest way to do this is with a multi-market for the total outcomes among these 93. Here is that market:

As I mentioned before, while there are 93 votes among these states, a fortunate alignment in the additive combinatorics means there are only 60 possibilities for the vote total. The market above tracks the probability for each of these breakpoints.

Crucially, the Democratic candidate needs to win 44 votes among the seven states to win the election. This gives us our first arbitrage opportunity: The 44 break-point on this market is a direct arbitrage for the main hypothetical binary market. The market is structured as a cumulative probability distribution, so it also implicitly provides an opportunity to arbitrage any higher vote-totals that have more probability than a lower vote-total.

The EV Count Portfolios

There is a further arbitrage opportunity that involves linking the vote total market to markets on the individual state probabilities, like Gabrielle’s:

The way this arbitrage works is by effectively creating two portfolios which pay off a value equal to the number of votes in the total.

The first way to create the portfolio is to purchase an amount of YES shares for each of the 7 states equal electoral college allocation. So I purchase:

11 YES shares in a market on whether the Democrat will carry Arizona

16 YES shares in a market on whether the Democrat will carry Georgia

15 YES shares in a market on whether the Democrat will carry Michigan

6 YES shares in a market on whether the Democrat will carry Nevada

16 YES shares in a market on whether the Democrat will carry North Carolina

19 YES shares in a market on whether the Democrat will carry Pennsylvania

10 YES shares in a market on whether the Democrat will carry Wisconsin.

Hopefully it’s clear that if you held all of these shares, the amount you would get paid out would be the total electoral vote count among the states.

But there’s a second way you can purchase this portfolio, using the cumulative distribution market:

Buy 1 YES share in the Democrat getting at least 1 electoral vote2

Buy 1 YES share in the Democrat getting at least 2 electoral votes

Buy 1 YES share in the Democrat getting at least 3 electoral votes…

… and so forth up to 93.

This portfolio also pays you out an amount equal to the total electoral vote count among the states, because all of the shares for outcomes less than or equal to the true total will pay off, and the outcomes above will not.

The fact that this portfolio can be realized in two separate ways means that there is an arbitrage opportunity: If the prices at which these portfolios can be purchased are different, then by buying the cheaper one and shorting an equivalent amount of the more expensive one, you receive a portfolio of shares which is ultimately risk-free, but which costs less than it’s worth.

Second Order: Arbitraging the Variance

What the above arbitrage guarantees, if there are enough traders to pick it up, is that the expected value of the distribution implied by the electoral vote count multi-market is exactly what one would predict from the individual probabilities on the state outcomes. This is nice because if we can correctly predict the expected value, we have a good sense of the distribution, and it’s more likely that the critical value of 44 is correct. What other properties of this distribution can we constrain with arbitrage?

A natural idea is to constrain the variance of the distribution. The variance is defined as

We already have constructed a portfolio that pays out X, and so we assume out prediction of the expected value is correct. The other part of the equation is the expected value of X2. In fact, we can make a portfolio that pays out the square of the electoral vote count just as easily as we can create on that pays out the electoral vote count itself, in much the same way:

Buy 1 YES share in the square of the Democrat vote count being at least 1

Buy 1 YES share in the square of the Democrat vote count being at least 2

Buy 1 YES share in the square of the Democrat vote count being at least 3

Buy 1 YES share in the square of the Democrat vote count being at least 4

These aren’t explicitly options, but the square of the vote count will be at least 1, 2, or 3, if the vote count itself is at least 1, and the square of the vote count will be at least 4-8, if the vote count itself is at least 2, and so forth. In each case, we can find a share in the multi-market that reflects the desired outcome.

How can we make this “square of the vote count” portfolio using pre-existing markets? In fact we can. Without going into the details, this portfolio can be bought by obtaining:

For every state, a number of YES shares equal to the square of the state’s vote allocation in the state going Democrat.

For every pair of states, a number of YES shares equal to the product of the vote allocation in both of the states going Democrat.

While the second type of market doesn’t exist as far as I can tell, it’s possible to get something equivalent from the individual states outcomes and a third market asking whether two states will vote the same way.

Luckily, there are only 21 ways to make a pair of states from our 7, so it’s not too hard to add any missing ones to Evan’s market.

Activating the Arb

We have a pretty good set of markets now, and a lot of ways to arbitrage between them. The only remaining challenge is to write a piece of code that will allow a users to detect and make these arbitrage trades. The trick with this is that it can be hard to determine what prices you can get for what volumes, given the complex construction of the portfolios, factoring in the presence of both AMMs and limit orders providing liquidity.

As a first step to this, I am writing an arbitrage bot which I am open-sourcing here. I may make another post about the bot itself at some point, but its main feature is its use of convex optimization (via the cvxpy python library) to determine how much of a particular user-defined portfolio can be bought at a certain price. This lets the bot compute from first principles the optimal purchases to make to complete an arbitrage of two portfolios of equivalent value.

The code at the GitHub link has already been operating intermittently over the past couple of weeks under the @JointBot username. Hopefully, it will continue to make a profit and price the 2024 political markets efficiently when I get around to describing the above arbitrages in cvxpy. Readers should feel free to download the bot and try it themselves, though no guarantees that a massive bug won’t eat your entire balance.

Happy trading!

If there is a 269-to-269 tie, then there is a tiebreak in the House of Representatives, which would likely go to the Republican candidate. There is also the possibility of faithless electors, which I don’t consider in this article.

Note that there does not explicitly exist an answer for in the multi-market for the Democrats getting 1-5 electoral votes because it is impossible to get these exact numbers of votes among these states. Because of this though, A share in one of these outcomes is exactly equivalent to a share in the Democrat getting at least 6 votes among the states, so you can just buy that.